All Categories

Featured

[/image][=video]

[/video]

Withdrawals from the cash money worth of an IUL are usually tax-free up to the quantity of costs paid. Any kind of withdrawals over this amount might go through tax obligations depending on policy structure. Typical 401(k) contributions are made with pre-tax dollars, lowering taxable earnings in the year of the payment. Roth 401(k) contributions (a strategy feature readily available in most 401(k) plans) are made with after-tax payments and afterwards can be accessed (incomes and all) tax-free in retirement.

Withdrawals from a Roth 401(k) are tax-free if the account has been open for a minimum of 5 years and the individual mores than 59. Properties taken out from a standard or Roth 401(k) before age 59 may sustain a 10% charge. Not precisely The cases that IULs can be your own bank are an oversimplification and can be misdirecting for several reasons.

Nevertheless, you may undergo upgrading associated wellness inquiries that can influence your ongoing costs. With a 401(k), the cash is always yours, including vested employer matching despite whether you give up contributing. Danger and Guarantees: Firstly, IUL policies, and the cash money value, are not FDIC insured like common savings account.

While there is generally a flooring to avoid losses, the development capacity is covered (meaning you might not fully gain from market upswings). Many specialists will concur that these are not equivalent products. If you want death advantages for your survivor and are worried your retired life cost savings will certainly not be sufficient, after that you may desire to take into consideration an IUL or other life insurance product.

Sure, the IUL can give accessibility to a money account, but once more this is not the primary purpose of the product. Whether you want or require an IUL is a very individual inquiry and relies on your main economic objective and goals. Listed below we will certainly try to cover benefits and limitations for an IUL and a 401(k), so you can further delineate these products and make an extra enlightened choice regarding the ideal means to handle retirement and taking treatment of your liked ones after death.

Iul Dortmund

Loan Costs: Car loans against the plan accrue passion and, otherwise paid off, lower the fatality advantage that is paid to the recipient. Market Involvement Restrictions: For most plans, financial investment development is connected to a stock market index, but gains are commonly covered, restricting upside possible - iul life insurance vs 401k. Sales Practices: These policies are commonly sold by insurance coverage representatives who might highlight advantages without completely explaining costs and dangers

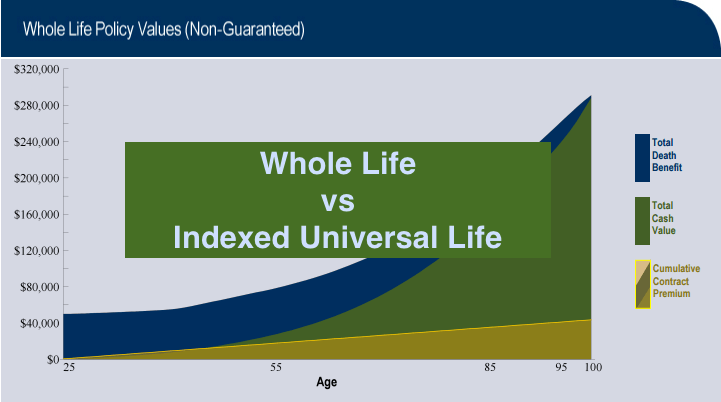

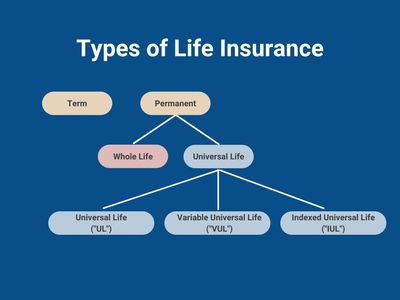

While some social media pundits suggest an IUL is a substitute item for a 401(k), it is not. Indexed Universal Life (IUL) is a type of permanent life insurance coverage policy that additionally uses a cash money worth component.

{kind=link}

Latest Posts

Fixed Indexed Universal Life Pros And Cons

Nationwide Indexed Universal Life Accumulator Ii

Iul Unleashed